What do the high banks know for tomorrow – supported by primary research

When I was in the bank, I always expected certain annual sellers meetings and reports. These key partners provided a valuable overview of what was happening beyond the four walls of our institution. Their contribution was essential to helping us appreciate our market position and refine our strategy.

Some of the most influential reports were from Bai Benchmarking, CSAT, Visa and Greenwich Associates. These sources included in our internal data and compared them to data from our industry peers – knowledge that we could not have entered otherwise.

That is why I’m excited about Intelligent Banks: Future Ahead, A new part of primary research by Impact Economist and Sas.

Based on a study of more than 1,700 senior banks worldwide, plus comprehensive research and deep interviews, our new report identifies the most pressing trends and challenges facing the financial services industry over the next decade and explores how those advantages are forming its future.

A continuation of Banking in 2035: three possible futureA popular report we released three years ago, our new report builds that foundation with fresh data, various executive perspectives and even more real -world knowledge. This blog post summarizes the main points from the latest report.

The weapons racing

While there were some distances and surprises, the results of the study reveal a wide approximation throughout the industry. Banks recognize shifts that require their attention and are responding by strengthening basic frameworks, evolving infrastructure, adopting and innovating new technologies, increasing talent and utilizing the skill of strong seller and partner ecosystems.

The generator (Genai) is emerging as a threat and a tool in the constant battle against fraud. While fraudsters increasingly exploit deepfaka and synthetic identities, 54% of banking executives cite the increasing complexity of fraud as their main concern. He’s powerful discovery keeps considerable promises, but high front costs and integration challenges continue to hinder adoption. Cloud-based services and embedded in the product modeling are seen as more cost-effective alternatives.

Essentially, fraud detection patterns rely on unified data, high quality-something that many banks still miss. Fragmentation of data through the silos remains an ongoing issue. To address this, the institutions need a stronger writing between the leadership and the “evangelists of it” within the business units to connect teams with the goals, skills and strategies of joint implementation.

Data Governance: From compliance to competitive advantage

The effectiveness of it is naturally linked to the quality and security of data. As a result, data governance is becoming a cornerstone of banking technology transformation. One-third of the executives list the governance frameworks-the politics that regulate the approach, quality and compliance of the data-the most effective tool to ensure data security, before automation and detection of the threat led by it.

Some banks are taking proactive steps, such as the pure DBS Bank framework (intentionally, startling, respectful, explanatory), to guide the use of ethical data. The governance agenda is also expanding to include ownership models, traceability and preparation for divisive technologies such as quantum computing. In particular, retail banks – with their large consumer data thresholds – express greater concern about data quality than their corporate counterparts.

Adjustment: The burden or catalyst?

While some governments are pressuring to free the heritage regulations, the regulatory landscape for it, the intimacy and sovereignty of the data is becoming increasingly fragmented. The EU’s act classifies the financial decision-making based on it as a “high risk”, while the US regulation remains divided into the state level. Most bank managers say they are less concerned about overloading and more focused on the need for clarity and harmonization.

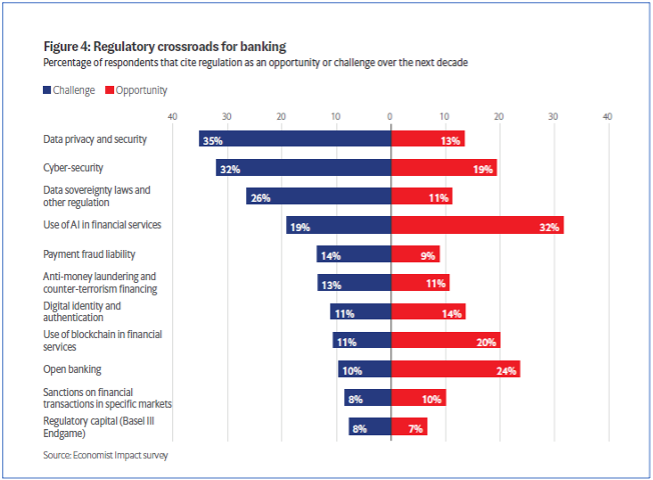

Despite increasing compliance costs-reported by more than 75% of respondents-thirds of executives believe that those costs are justified, given the reputable and legal risks of disrespect. Looking forward, the three main areas of regulatory friction over the next decade include data privacy, online security and data sovereignty (see Banking Crossroadsan excerpt from the report, below).

To manage the increasing complexity, banks are increasingly investing in compliance automation, while also promoting deeper cross-functional cooperation between technical teams and compliance. Institutions as aspires have restructured internal teams to better connect these historically silent functions.

Fall of Competition: From Fintechs to CBDCS

Traditional banks are facing an existential threat on numerous fronts: fintechs, only digital bank, Big Tech and now the digital coins of the Central Bank (CBDCS). While fintechs continue to expand to payments and credit markets, Big Tech entry through mobile wallets and embedded finances signal deeper interruptions.

At the same time, CBDC pose a unique risk by potentially disappearing banks enabling consumers to hold deposits directly with central banks. Although many see CBDCs as a long-term threat, their potential to erode deposit bases, limiting borrowing capacity and disruption of international payment flows should not be underestimated. As a result, strategic planning about digital assets – including custody services and cryptic risk management – is becoming an increasing advantage.

Innovation models: Build, buy or partners?

To stay important, banks must embrace continuous innovation – not only through the adoption of technology, but through cultural transformation. As M&E activity continues, most leaders see internal innovation and employee setting up as the most effective strategy. Purchases often fall short due to the challenges of cultural integration and misinformation.

Partnerships are increasingly seen as the most effective model for running innovation. Cooperation with Fintechs and Big Tech enables banks to escalate offers, achieve new segments of clients and developing technology without heavy investment in the front.

However, these partnerships can also present new risks. Data sharing with third parties is a high security concern, and internet security discrepancies and compliance practices can expose banks to fraud and regulatory violations. Common Governance Committees and Framework such as Financial Data Exchange (FDX) can help institutions maintain supervision and accountability within these complex ecosystems.

Priorities for bank managers

To navigate forward instability, banks must approximate risk, technology and innovation strategies around five imperatives. I will not discover everyone here – you can see the full list and knowledge of experts in the full report.

On the contrary, I will share two strategies that are close to my heart as an internal industry.

First, it is very important for banks to strengthen data governing and its governing. This includes the construction of powerful frames with clear ethical supervision, responsibility and auditability of the model. “Having a strong governance framework is not optional,” says Zechariah Akinpelu, the leading information security officer in Bank Unity.

It is also necessary for the financial institutions to gain customer confidence. A distinctive sign of traditional banks, faith now requires a wider engagement. From transparency in decisions directed from him to protection of sensitive data and constantly trying to improve the customer’s experience, banks need to show that they are acting on the best interests of customers at any point of touch.

As technologies mature and the regulatory perimeter evolves, banks must move beyond the growing change. Success in this new era requires risk leaders who can help reshape functioning models, predict threats, and turn compliance and governance into competitive advantages.

But don’t just take my word for it. There are many more data, details and comments from industry experts to Intelligent Banks: Future Ahead. Complete report also includes case studies from standard Chartered, DBS, revolt, clarna and JPMORgan.

I hope that this new primary research inspires fresh thinking or prove the strategies you are already forming in your institution just as similar penetrations once made me.